Smart taxpayers file and pay taxes on time and know various ways to save money on taxes. The Indian government offers several tax exemption and deduction policies to help people save taxes. However, only a few people know about it. For example, many people claim income tax deductions for home loan interest payments or House Rent Allowance (HRA), but they don't know that they can claim both if certain conditions are met and determined. The article goes through the areas on how to claim HRA and home loan tax benefits.

| Table of Contents: |

Can a Taxpayer Claim both HRA and Home Loan Tax Benefits?

Among tax-free options, House Rent Allowance (HRA) is one of the main ways to reduce tax liability. On the other hand, home loans can also benefit from tax exemptions. But is it possible to avail of HRA benefits and tax deduction benefits on home loans at the same time and how to claim HRA and home loan tax benefits? Technically it is possible, but you have to pay attention to the procedure followed to claim that tax benefit.

Benefits of HRA and Home Loan Exemption

HRA will be offered at the lowest of the following provisions under Section 10 (13A) of the Income Tax Act 1961:

- The employer permits HRA.

- Employees who live in the metro area will receive 50% of their basic wage; otherwise, they will receive 40% of their basic salary.

- 'Less' actual rent paid 10% of base salary (plus DA and eligible commission).

Tax Break for Home Loan Interest Payments

The EMI for a home loan includes both principal and interest payments. Taxpayers can claim a deduction of up to 2 lakhs on the interest component in a year under Section 24(B) of the Income Tax Act 1961. A home loan interest rate calculator will assist you in calculating your interest costs and claiming any appropriate deductions.

How to Claim Both HRA and Home Loans?

Simply put, people who own a home and claim a tax deduction for home loan interest payments cannot claim an HRA exemption. However, if a homeowner pays a Home Loan and receives HRA as part of their salary, they can receive both benefits in the following scenarios which mention how to claim both HRA and home loan tax benefits:

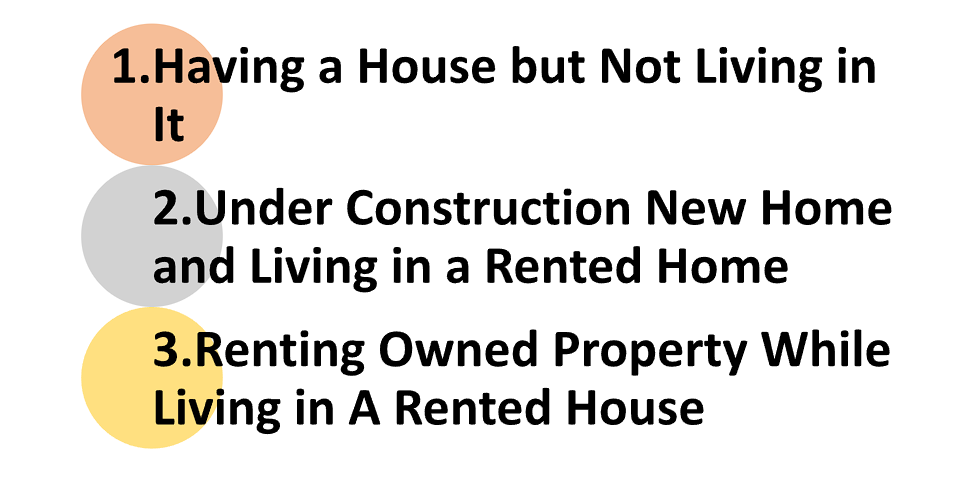

- Having a House but Not Living in It: If you have a loan for a residential property but live in another residence for which you pay rent, you can claim available tax benefits for both the HRA and the residence Loan. The stipulation is that both rented and owned property be located in different cities.

You must also provide a cause for not residing in your own home, which can be a job location that is different from your home location, a long distance from home to office, a transfer from your home location to another city, or any other justifiable reason.

- Under Construction New Home and Living in a Rented Home: This is one of the most prevalent circumstances, since you may have taken out a loan for a residential project that is still under construction, so you live in a leased property until your own home is finished. In such a circumstance, the advantage of both Home Loan tax deductions can be claimed.

The limitation is that a claim may only be filed for interest repayment, and you can collect such deductions in 5 equal payments over the next 5 years after completion. In such a circumstance, you are not permitted to claim a deduction for principal repayment. HRA may be claimed till completion by your city and wage breakdown as described above. - Renting Owned Property While Living in A Rented House: In this instance, you can claim a tax deduction for both the home loan and the HRA. There could be various reasons for renting out your owned property, including the need for a larger home, relocating your office to a more distant area from your home, or a similar shift in preferences. You will be expected to provide rental revenue from rented-out property, which will be taxable at the applicable rate. As your limit specifies, you can claim HRA.

Things To Keep in Mind

Whatever your position may be, given there is scrutiny by the Income Tax department, you need to have valid reasons to support your filings. You need to make sure that when the Income Tax department sends you a notice to explain the reason for not occupying your own home and claiming the HRA, you should be able to prove your position with good reason. If you are unable to meet their concerns, you may be issued notifications.

End Note

A salaried person who receives HRA as part of their income and pays EMIs on their home loan can take advantage of both HRA exemption and home loan interest or principal repayment deduction. However, to obtain the benefits, they must meet the conditions outlined in this article. If the taxpayer's case is eventually picked up for investigation by an income tax officer, they should be prepared to verify their deductions if questioned.

In case of any query regarding how to claim HRA and home loan tax benefits, feel free to connect with our legal experts at Legal Window at 72407-51000.

Company Secretary and diligent learner deeply immersed in the world of corporate law, compliance, and governance with a focus on developing a robust foundation in legal principles and corporate practices. Passionate about exploring the intricacies of company law, regulatory compliance, and corporate governance.

Categories

- Agreement Drafting (23)

- Annual Compliance (13)

- Change in Business (37)

- Company Law (150)

- Compliance (90)

- Digital Banking (3)

- Drug License (4)

- FEMA (17)

- Finance Company (42)

- Foreign Taxation (9)

- FSSAI License/Registration (15)

- GST (124)

- Hallmark Registration (1)

- Income Tax (214)

- Latest News (36)

- Miscellaneous (170)

- NBFC Registration (8)

- NGO (18)

- SEBI Registration (6)

- Section 8 Company (10)

- Start and manage a business (27)

- Startup/ Registration (134)

- Trademark Registration/IPR (48)

Recent Posts

- Major Upgrade: Breaking Down GST 2.0 September 15, 2025

- New Income Tax Bill 2025 August 27, 2025

- ITR-3 Form Explained: Who Should File & Step-by-Step E-Filing Guide (FY 2024-25) June 25, 2025

All Website Tags

About us

LegalWindow.in is a professional technology driven platform of multidisciplined experts like CA/CS/Lawyers spanning with an aim to provide concrete solution to individuals, start-ups and other business organisation by maximising their growth at an affordable cost.

Ask an Expert

")

")

FILING GUIDE FOR blog cover image (1)")

ITR-1 (Sahaj) Filing Guide for FY 2024-25: Who Should File & How to E-File Step-by-Step (AY 2025-26)